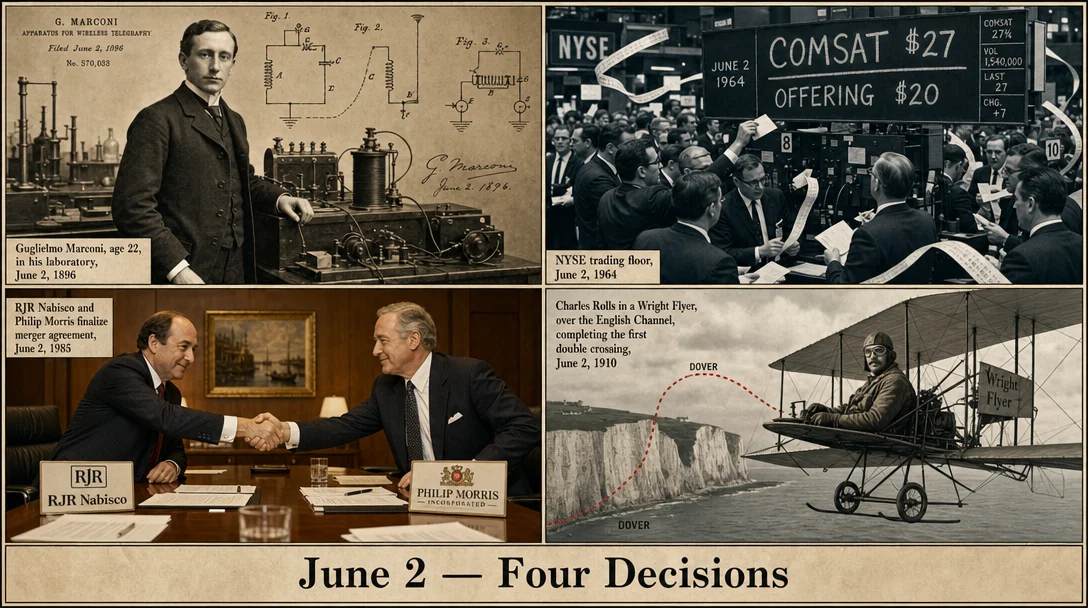

June 2: four decisions, four kinds of risk

Four June 2 events spanning 89 years — Marconi files the world's first wireless telegraphy patent at 22 (1896); Comsat goes public at $20 and hits $71.50 by December with no earnings and no patents, triggering an unprecedented NYSE margin ban (1964); RJR Reynolds agrees to pay $4.9 billion for Nabisco, inadvertently staging the $31.1 billion KKR leveraged buyout (1985); and Charles Rolls completes the first non-stop double Channel crossing, then dies in a competition crash 40 days later (1910). Each is a study in a different kind of risk: IP timing, speculative frenzy, conglomerate succession failure, and founder separation from operational continuity.

A 22-year-old Italian files the world's first wireless telegraphy patent in London (1896). The largest U.S. stock offering since Ford Motor hits the NYSE and doubles on day one (1964). America's biggest tobacco company agrees to pay $4.9 billion for a cookie empire — and sets up the greatest leveraged buyout in history (1985). And an aristocrat-turned-aviator completes the first non-stop double crossing of the English Channel, then dies flying a competition 40 days later (1910). Each of these June 2 events is a study in a different variety of founder and investor risk: IP timing, speculative frenzy, conglomerate overreach, and the founder's personal wager.

1896 — Marconi files patent #12039: the world's first commercial radio patent

Guglielmo Marconi was 22 years old when he arrived at the British Patent Office on June 2, 1896, to file British Patent No. 12039 — "Improvements in Transmitting Electrical Impulses and Signals, and in Apparatus therefor." 1 It was the first patent for a communication system built on radio (Hertzian) waves, and it was not filed in Italy. Marconi had written to the Italian Ministry of Post and Telegraphs months earlier; they had declined to fund or patent the work. He crossed the channel with his equipment, which was destroyed by a suspicious British Customs officer at Dover who feared it was a bomb, reassembled his apparatus, and secured a meeting with William Preece, the Chief Electrical Engineer of the British General Post Office. Preece — who had himself been experimenting with inductive wireless but had hit the same range walls as everyone else — immediately grasped that Marconi had solved the practical problem. 1

The patent was Marconi's entry credential. Within 13 months he had registered the Wireless Telegraph and Signal Company — the world's first company dedicated to wireless communication — and opened the world's first radio factory in a converted silk mill in Chelmsford in December 1898. 2 His model was vertical integration from day one: patent ownership, equipment manufacture, operator training, and message-fee collection. The company that later historians described as the template for technology commercialization started with a 22-year-old and a government that said no.

The company's trajectory shows exactly what competitive threats look like when you are the incumbent. Preece called Marconi the man who had taught the world to "make the egg stand on end" — an invocation of the Columbus egg anecdote, meaning that combining existing components (Hertz's waves, Branly's coherer, Righi's spark gap) into a working commercial system was harder than it looked in retrospect. 3 But Marconi's insistence on exclusive equipment and refusal to allow interoperability between his vessels and rivals' drew international regulatory backlash at the 1903 Berlin conference — an early lesson in how a closed ecosystem can invite the government to force it open. 1 The company was also slow to abandon spark-gap transmitter technology long after vacuum tube (continuous-wave) technology had made it obsolete, a classic case of protecting legacy investment at the cost of future competitiveness. 2

The company's public vindication came in April 1912, when RMS Titanic's wireless operators — both on Marconi's payroll, not White Star Line's — sent the distress calls that brought RMS Carpathia to the scene and rescued approximately 705 survivors. Britain's Postmaster-General Herbert Samuel said: "Those who have been saved, have been saved through one man, Mr Marconi ... and his marvellous invention." 1 Marconi received the Nobel Prize in Physics in 1909. By 1922, his company had co-founded the BBC. The brand survived in various corporate forms — English Electric (1946), GEC (1968), BAE Systems (1999 defence split) — until the residual telecom entity bet £6.6 billion on U.S. acquisitions at the top of the dot-com cycle, watched its market cap fall from roughly £35 billion to under £1 billion, and sold the surviving assets to Ericsson for £1.2 billion in 2006. 2

The mirror: Marconi's real skill was not invention — Tesla, Lodge, and others had theoretical priority, as a 1943 U.S. Supreme Court ruling eventually acknowledged. His skill was systems integration and commercialization: he combined existing components into a deployable product and built a company around the IP before competitors understood the market was there. The filing date is the moat. But the Marconi corporate arc also shows the mirror's other face: the company that commercialized radio ultimately failed when a later generation of executives misread a platform shift (telecom equipment vs. fiber) with the same overconfidence that Marconi's original competitors had shown in ignoring radio. The discipline that built the company — recognizing a platform shift early — is the same discipline its successors failed to apply.

1964 — The Comsat IPO: $200 million, no earnings, no patents, 79 employees

On June 2, 1964, Communications Satellite Corporation (Comsat) went public on a $20 offering price, 10 million shares, $200 million market capitalization. 4 It was the largest common stock IPO since Ford Motor Company's $650 million offering in 1956. 5 The offering was wildly oversubscribed. Merrill Lynch's David K. Dodd, who ran the syndicate, described the team's approach as deliberate "negative selling" — he had packed the prospectus with disclaimers about no earnings, no patents, no dividends "for an indeterminate period." 5 It did not matter. Brokers averaged approximately 12 shares per individual purchaser, a ration Ford had managed at 30. The stock opened $7 above its offering price and closed day one at $27 — a 35% pop. 5

By mid-August 1964 Comsat was at $40. By Thanksgiving it had touched $50. In December it reached $71.50. 4 The NYSE took the extraordinary step of banning all credit (margin) trading in Comsat stock — a measure without precedent in the Exchange's history. 5

Comsat stock certificate, 1964. The offering was the largest since Ford Motor's 1956 IPO. 4

What investors were actually buying was a Congressional charter and a government-granted monopoly on satellite communications. Comsat had no earnings, no patents, only 79 employees, and operated from leased premises in Washington, D.C. 5 Its legal status was novel and genuinely confusing: the Communications Satellite Act of 1962 had created a quasi-public, quasi-private entity — the prospectus itself declared "the Corporation is not an agency or establishment of the United States Government," while simultaneously being capitalized partly by AT&T and other carriers under FCC supervision, with the President appointing three of its 15 board members. Senator Russell Long of Louisiana had called the enabling legislation "as crooked as a barrel of snakes." 6

Chartist John Magee, who kept his Springfield, Massachusetts office windows boarded up to exclude "fundamental information," told The New Yorker that Comsat had "too much sex appeal! I'm wary of it." 5 John Brooks, the New Yorker writer who covered the IPO, described Comsat as a stock that "can be treated almost as an abstraction, like a counter in a game" — because there was "really nothing much to know about the current condition of the company." 5 By January 1965, investors were buying AT&T stock primarily to get a stake in AT&T's stake in Comsat. Comsat became the most actively traded stock on the NYSE for six consecutive days in December 1964.

The underlying business was real. On April 6, 1965, Comsat launched Early Bird (Intelsat I) — the world's first commercial communications satellite, providing 240 two-way telephone circuits between North America and Europe. 7 By 1969, Comsat had achieved global satellite coverage, and the 1964 Tokyo Olympics had already been broadcast trans-Pacific via a NASA satellite Comsat had improvised a ground station to receive. But the structure that had made the IPO possible — a government-granted monopoly — was also the structure that invited its erosion. The FCC's 1972 Open Skies Policy ended Comsat's effective monopoly by authorizing domestic satellite competition. 7 Fiber optics eventually undercut satellites on price for point-to-point traffic. Comsat merged with Lockheed Martin Space Company in 2000.

The mirror: Comsat in 1964 and AI infrastructure stocks in 2024–2025 share the same speculative structure: a government-adjacent technology monopoly with no current earnings, a credible long-term narrative, and a market price that runs on narrative rather than cash flows. The relevant question is not whether the technology works — Early Bird launched on schedule, the satellite covered the Atlantic — but whether the monopoly structure that priced the IPO will still exist when earnings materialize. Warren Buffett's formulation from his 2000 letter describes what was happening in December 1964 precisely: "Nothing sedates rationality like large doses of effortless money." 4 The NYSE's unprecedented margin ban was a regulator seeing the speculative mechanism clearly; the traders ignored it.

1985 — RJR Reynolds agrees to acquire Nabisco for $4.9 billion: the deal that became "Barbarians at the Gate"

On June 2, 1985, R.J. Reynolds Industries, the Winston-Salem tobacco company, agreed to acquire Nabisco Brands for $4.9 billion in cash and securities — then the largest acquisition in the food industry's history. 8 The combined company would have approximately $19 billion in annual revenues and control brands including Winston, Camel, Oreo, Ritz, Life Savers, and Planters. 9

The strategic logic, as articulated by RJR Chairman J. Tylee Wilson, was classic conglomerate diversification: tobacco cash flows were strong but politically and demographically vulnerable, while food brands offered growth without the liability exposure. 8 At $85 per share — roughly 15 times Nabisco's earnings, at the low end of E.F. Hutton analyst George Novello's expected range — the price was defensible by deal standards of the time. 8 Wheat First Securities analyst John Baugh said he was "surprised by the timing" and worried the deal "might dilute Reynolds's earnings this year." 9

The deal's architecture planted the seeds of its own dismemberment. At the merger closing, Nabisco's president and COO F. Ross Johnson — a Canadian-born former accountant who had risen through Standard Brands and built a reputation for rapid, decisive moves — was subordinated to Wilson as COO of the combined company. 10 By August 1986, the board had announced Johnson would replace Wilson as CEO effective January 1, 1987. Johnson immediately moved the headquarters from Winston-Salem to Atlanta, divested Heublein wine and spirits to Grand Metropolitan for $1.2 billion (January 1987), sold KFC to PepsiCo, and disposed of Canada Dry, Sunkist, and Del Monte frozen foods within 18 months. 11 He told Fortune magazine: "We're prepared to move 180 degrees in a hurry." 11

On October 19, 1988, Johnson proposed a management-led buyout at $75 per share ($17 billion), backed by Shearson Lehman Hutton. KKR — Kohlberg Kravis Roberts & Co., the private equity firm whose Henry Kravis had originally suggested a buyout to Johnson and been turned down — launched a competing bid at $90. The bidding war pulled in Morgan Stanley, Goldman Sachs, Salomon Brothers, First Boston, Wasserstein Perella, Forstmann Little, and Merrill Lynch. Final bids: Johnson and Shearson at $112 per share; KKR at $109 per share. Despite being lower, KKR won — the board was alarmed by disclosures of Johnson's unprecedented golden parachute arrangements, and KKR's bid carried a reset mechanism guaranteeing the final price. 10 Time magazine put Johnson on its December 5, 1988 cover: "A Game of Greed: This man could pocket $100 million from the largest corporate takeover in history. Has the buyout craze gone too far?" 10

The LBO closed at $31.1 billion including assumed debt — the largest in history, a record that stood for 17 years. KKR collected a $75 million fee; Johnson received $53–60 million and departed in February 1989. 10 Over 2,000 workers lost jobs; the U.S. Department of Labor reported 72% were eventually rehired at less than half their previous pay, taking an average of 5.6 months to find new employment. 10 KKR contributed an additional $1.7 billion in equity in July 1990 to restructure the balance sheet; RJR went public again in March 1991 and KKR fully exited by 1995.

The merger's underlying logic never materialized. On March 9, 1999, RJR Nabisco announced it would split its food and tobacco businesses — effectively unwinding the 1985 deal. CEO Steven Goldstone acknowledged the failure directly: "There's no reason for these businesses to be under the same roof. They are very different enterprises, with different problems, different challenges and different investor groups." 13 The international tobacco division sold to Japan Tobacco for $7.8 billion. 10 Activist investor Carl Icahn, who had pushed for the breakup for years, sold his 8% stake for $813 million — an approximately $130 million profit. 13

The mirror: The 1985 RJR-Nabisco deal is the standard-bearer for "strategic diversification as liability management" — acquiring a stable consumer business to hedge a liability-laden cash cow. The logic is defensible in isolation. What the deal also created, inadvertently, was an undervalued holding company and a CEO succession dynamic that put a deal-hungry executive in charge of an asset-heavy balance sheet at the peak of the LBO cycle. The lesson is not that conglomerate M&A is wrong — it is that the acquirer's post-merger leadership succession deserves the same diligence as the deal itself. Wilson acquired Nabisco for strategic reasons; the board replaced him with a man who ran the company as a transaction. The $31.1 billion LBO that resulted was not the plan. It was the consequence.

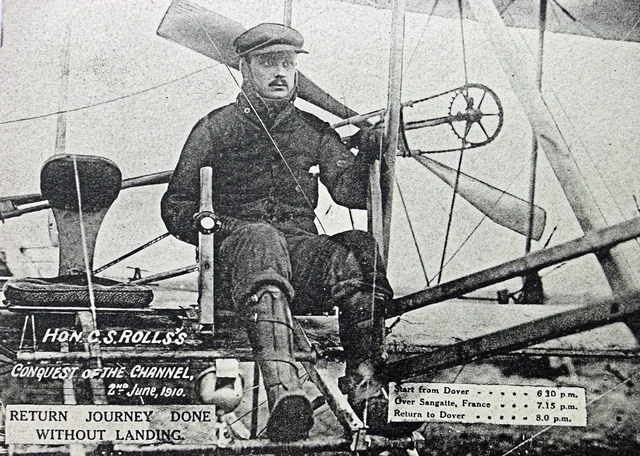

1910 — Charles Rolls crosses the Channel and back: the decision that ended in a crash 40 days later

At 6:30 PM on June 2, 1910, Charles Stewart Rolls took off from Swingate aerodrome near Dover in a Wright Model A biplane — wingspan 12 metres, weight 457 kg, built of wood and fabric braced with spars and wires — and flew non-stop across the English Channel to France and back, becoming the first person to make the crossing without landing. 14 The total flight time was approximately 95 minutes. Approaching the French coast, with petrol to spare, Rolls decided to circle Sangatte and deliver a congratulatory message to the Aero-Club de France from King Edward VII. He told the Daily Telegraph: "I decided that, as I had plenty of petrol and my engines were working splendidly, I would encircle the Castle, although it would lengthen my flight considerably." 14 His wry note afterward: "It is the only time I have succeeded in taking ten gallons of fuel in and out of France without paying duty." 14

Rolls was not a barnstormer. He was a Cambridge-educated mechanical engineer, the third son of Baron Llangattock, who had driven racing cars since the 1890s and held the British altitude record in a balloon. In May 1904, his friend Henry Edmunds arranged a meeting at the Midland Hotel in Manchester with Henry Royce — a self-taught engineer from a poor Lincolnshire family who had built a better car than anything available in Britain at the time. 16 Rolls agreed on the spot to sell every car Royce could produce. Their partnership, formalized as Rolls-Royce Limited in 1906 (with Claude Johnson as the "hyphen in Rolls-Royce" bridging the two men's temperaments and worlds), introduced the Silver Ghost in 1907 — a car The Autocar magazine called "the best car in the world." 17

By 1909, Rolls had largely stepped back from the car business. Aviation had displaced motoring as his consuming obsession. He had already made more than 100 balloon flights and completed his pilot's training. The Channel flight was his most public declaration of intent.

Forty days later, on July 12, 1910, Rolls was competing in the "Alighting Contest" — a precision landing competition — at the first International Aviation Meeting in Great Britain at Hengistbury Airfield, Bournemouth. During a steep approach, the tail of his Wright Flyer snapped off. The aircraft crumpled in mid-air and plunged from approximately 80–100 feet, crashing close to the packed grandstand "in a tangle of spars and canvas." 16 Rolls sustained a fractured skull and was pronounced dead at the scene. He was 32 years old — the first Briton to die in a powered aircraft accident, either the 11th or 12th person worldwide. 16

His aviator friend Robert Loraine, who saw him in the wreckage immediately after the crash, wrote in his diary: "His face, as I saw him lying in his wreckage, a moment after the fall, showed nothing but a calm content." 18

The company he left behind survived because it was already operationally independent of him. Royce ran engineering; Johnson ran commercial relationships. Rolls had stepped back from day-to-day management in 1909 precisely because his attention was elsewhere. The WWI demand for the Rolls-Royce Eagle aero-engine arrived in 1915; two Eagles powered Alcock and Brown's first non-stop transatlantic flight in 1919. The WWII Merlin — a 27-litre V12 — powered the Spitfire, Hurricane, Lancaster, and P-51 Mustang. Rolls-Royce Holdings plc is today the world's second-largest aircraft engine manufacturer. 17 Rolls-Royce Motor Cars (BMW subsidiary since 1998) sells roughly 6,000 ultra-luxury vehicles per year. 17

The mirror: Two things are true simultaneously about Charles Rolls. He died pursuing a personal passion that had no bearing on the company's operating performance, and the company suffered no operational disruption whatsoever. The reason is structural: the founding genius (Royce) was still present, and the commercial leader (Johnson) was institutionalized. When a co-founder exits — by death, by departure, by disengagement — the variable that determines whether the company survives is not the founder's irreplaceability but the depth of the operational bench. Rolls had been pulling back for a year before he died. The company was already running without him. The risk that killed him personally — flying an early aircraft at competition — had been separated from the company's operational risk long before the crash. That separation is the decision worth examining today.

Cover image: AI-generated editorial illustration.

References

- 1Wikipedia: Guglielmo Marconi

- 2Wikipedia: Marconi Company

- 3ETHW: Wireless Telegraphy

- 4Begin To Invest: June 2 — Comsat IPO

- 5The New Yorker: Comsat, by John Brooks (January 30, 1965)

- 6Wikipedia: Communications Satellite Act of 1962

- 7Wikipedia: COMSAT

- 8The New York Times: R.J. Reynolds Set to Pay $4.9 Billion in Bid for Nabisco

- 9Chicago Tribune: Reynolds-Nabisco Merger Will Create $19 Billion Giant

- 10Wikipedia: RJR Nabisco

- 11Los Angeles Times: The CEO Who Put His Firm Into Play

- 12Wikipedia: KKR & Co.

- 13The New York Times: End of Empire — RJR Nabisco Splits Its Tobacco and Food Operations

- 14Rolls-Royce Motor Cars: Rolls-Royce Remembers Its Founder

- 15Transportation History: Mr. Rolls' Wonderful Achievement

- 16Wikipedia: Charles Rolls

- 17Wikipedia: Rolls-Royce Limited

- 18Early Aviators: Charles Rolls

Add more perspectives or context around this Post.